Erdogan’s Gulf tour secures foreign investment pledges, crucial for Turkey’s depleted reserves ahead of large debt repayments in November…reports Asian Lite News

Turkish President Recep Tayyip Erdogan, after clinching another five-year term in the recent elections, last week embarked on an effort to save Turkey’s faltering economy by making a tour of Saudi Arabia, Qatar and the UAE, seeking investments and financial support from the oil-rich Gulf states.

The importance of a Gulf lifeline for Turkey’s ailing economy is shown by the fact that recently Qatar and the United Arab Emirates provided Turkey with a USD 20 billion currency swap, while Saudi Arabia last March deposited USD 5 billion into the Central Bank of Turkey. Furthermore, last month UAE and Turkey signed a trade deal amounting to about USD 40 billion over the next five years.

As the Turkish economy is facing runaway inflation close to 40 per cent, the Turkish Lira has lost more than 29 per cent of its value this year and foreign exchange reserves are depleted, Erdogan was reluctantly forced to accept economic reality and abandon, at least temporarily, his controversial economic policies.

He brought back to the post of Finance Minister former investment banker Mehmet Simsek, who had served in the same post from 2009 to 2015, and appointed Hafize Gaye Erkan, former CEO of First Republic Bank, as Governor of the Central Bank, trying to convince international investors that he will no longer insist on applying his unorthodox economic policies.

Erdogan’s tour of the three Gulf States had been prepared by Mehmet Simsek, who last month had meetings in Saudi Arabia, the UAE and Qatar and held preliminary discussions for the promotion of economic partnerships between these states and Turkey.

Speaking to reporters before leaving Istanbul, Erdogan said: “We hope to improve our relations and cooperation in many fields. We will focus on joint investment and commercial initiatives we can carry out together with these countries.”

The Turkish President, accompanied by about 200 businessmen and several Ministers, started his three-day tour on Monday, visiting first Saudi Arabia and having meetings with King Salman and Crown Prince Mohammed bin Salman.

In Jeddah some 400 business leaders and officials took part in the “Saudi-Turkish Business Forum” and discussed investment opportunities, particularly in the sectors of manufacturing, construction, tourism, mining, food agriculture and defence.

The two sides signed nine agreements covering energy, construction, digital technology, media, education, health and real estate. The value of these agreements has not been disclosed.

Saudi Defense Minister Prince Khalid bin Salman said that Saudi Arabia has agreed to purchase Turkish Baykar drones, but did not disclose the amount involved in the deal.

It should be noted that last month, Saudi giant company Aramco, a leading producer of energy and chemicals, held a meeting with some 80 Turkish contractors and discussed with them the prospects of many projects to be executed in Saudi Arabia for an estimated amount of USD 50 billion.

Currently, there are 1,140 Saudi companies operating in Turkey, and 395 Turkish companies investing in the Kingdom.

The next stop of President Erdogan was in Qatar on Tuesday, where he was greeted by Emir Shiekh Tamin Bin Hamad Al Thani and had talks at the Lusail Palace.

During the meeting, Erdogan gave the Emir as a gift Turkey’s first manufactured electric car called Togg.

The two leaders attended the signing of a joint statement between Qatar and Turkey on the occasion of the 50th anniversary of the establishment of diplomatic relations between the two countries.

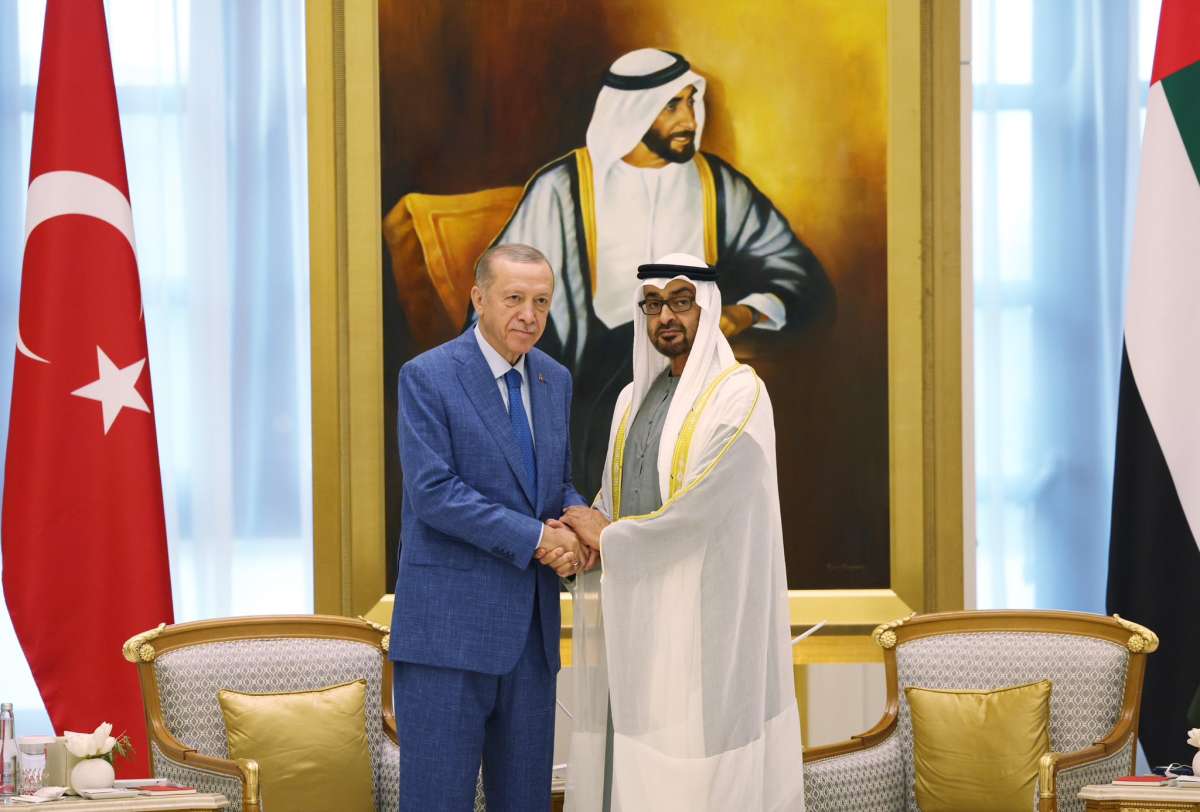

In the last stop of Erdogan’s tour on Wednesday, UAE President Sheikh Mohammed bin Zayed Al Nahyan met with Erdogan at the presidential palace in Abu Dhabi.

According to the official WAM news agency, the two leaders attended the signing of agreements and memorandums of understanding “estimated to be worth USD 50.7 billion.

The Abu Dhabi Developmental Holding sovereign wealth fund (ADQ) alone signed a memorandum of understanding to finance up to USD 8.5 billion of Turkey earthquake relief bonds and to provide $3 billion in credit facilities to support Turkish exports.

President Erdogan’s tour of the three rich Gulf countries can be considered a successful one, as he secured pledges of sizeable direct foreign investment and desperately need foreign exchange to boost the Central Banks’ depleted foreign exchange reserves, before November when Turkey is facing a number of large debt repayments. (ANI)

ALSO READ-UK announces £680m for high-speed electric railway in Turkey